This is your TSP Watchdog UPDATE for the week ended August 23, 2019.

Stocks fell for a fourth week in a row. The S&P 500 lost 1.44%. The Dow fell 0.99%. The NASDAQ dipped 1.83%.

We almost made it to a nice gain for the week – until Fri.

Thu night, we sat on 1%, or more, gains in all three indexes. Then, Fri morning, China announced tariffs on $75 million of US imports. President Trump quickly announced that the US would respond – but did not immediately announce what the response would be. The markets were left to imagine the worst, and that they did. The Dow dropped 623 points.

No official announcement of the US response to China’s tariffs came until after the markets closed. The new and increased tariffs that were finally announced late Fri will be sorted through on Mon. At this writing, overnight stock futures are UP – but that is not always an indicator of what trading will be in the morning.

Beyond Friday’s drubbing, stocks had a good week on the back of lukewarm (mixed) economic reports. Manufacturing numbers continue to look soft (pretty much a direct impact of the trade wars) while the housing sector showed better than expected.

There was also another brief inversion of the yield curve on Fri – with the interest rate on the 10-year treasury dipping below the rate on the 2-year. Even though this inversion was short-lived, it is an indicator that scares many on Wall Street as a precursor to recession.

There were also a few earnings reports during the week – which were generally solid.

The unsettled, mixed-results economy we are seeing today is a far cry from the undeniable growth machine we saw in 2017 and 2018. The uncertainty of the current picture does not help stocks. Remember, in some ways, uncertainty is worse for investors than actual bad news; it leaves them worrying about the worst.

As long as the news bounces back and forth – good-bad, good-bad – don’t expect stock prices to do much. There may be spikes up, but don’t expect them to be lasting.

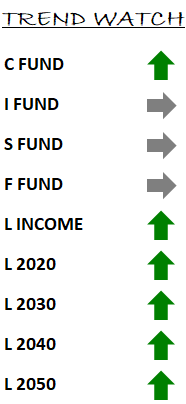

In our TSP Watchdog database, we have price movements but not quite trend changes.

The S fund dropped right down to its trend line. Any further declines will signal a negative trend in the S fund, but we’re not quite there yet.

The I fund, which dropped right down to its trend line last week, actually gained a few pennies during the week (remember, the I fund is International stocks – so it does not always move the same direction as its US stock counterparts, the C fund and S fund). It remains right at its trend line.

Of the growth funds, only the C fund remains above its trend line – though it is getting closer.

The F fund remains right at its trend line – but still just below it. Bonds have rallied as interest rates around the globe fall, but the F fund has continued to fall just short of a positive trend. This may prove fortuitous, as some inflation data (which often foretells of weakness in bond prices) is beginning to line up towards rising inflation.

Sometimes it is surprising when a HUGE decline does not trigger negative trends. Candidly, I expected some negative trends after Friday’s selloff. But the fact that we don’t have any new negative trends to report is testament to the strength of the positive trends that we have had for the past few years.

With the I fund and S fund sitting right on their trend lines, any further declines will trigger negative trends. The C fund does not have much “cushion” left before it falls onto a negative trend. Bottom line, we are at a make-it-or-break-it point. If stocks do not rebound from here, we will see negative trends take hold. If/when that happens, we will alert you.

These are the tough times in the market when we earn our keep. If the current volatility develops into new negative trends, we will let you know so you can take appropriate action.

Of course, when things get bumpy like this, a lot of folks have questions. We encourage you to send them over. We will reply ASAP.

Scot B.